Advice Processes & Sales & Marketing for Professional Services & Strategic Issues

Not All Customers Are Good Advice Clients

November 17, 2023

“All customers are good advice clients”…or are they?

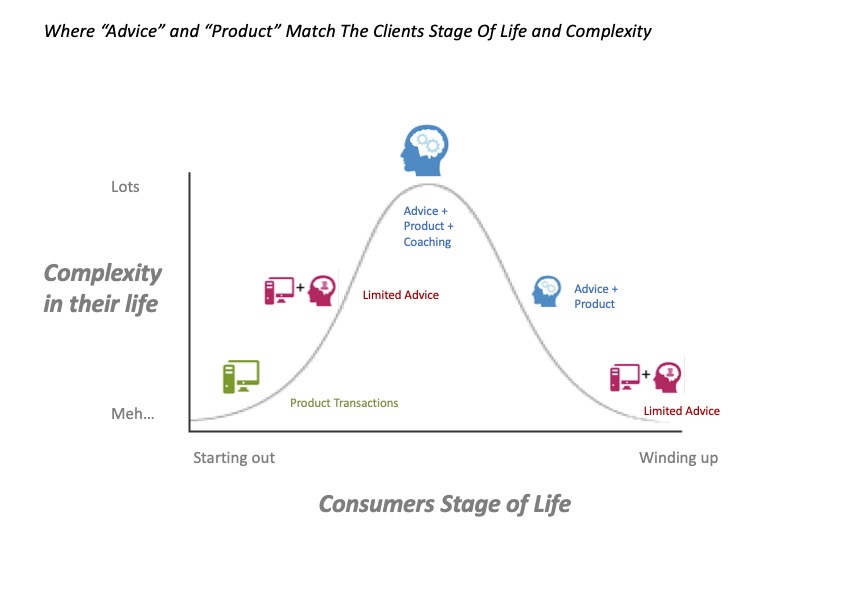

“All customers are good advice clients”…or are they? While it is not absolute correct for all consumers all the time I do believe that this is generally correct for the majority of consumers. That is, early in life their needs are few and relatively simple. Later in life their needs are relatively few (compared to prior working years), and more often than not the ongoing advice is extremely limited in scope or fairly simple.

While it is not absolute correct for all consumers all the time I do believe that this is generally correct for the majority of consumers. That is, early in life their needs are few and relatively simple. Later in life their needs are relatively few (compared to prior working years), and more often than not the ongoing advice is extremely limited in scope or fairly simple.

Comments (0)