Practice Management & Strategic Issues

Why Advisers Need To Invest In Their Businesses. Now.

July 16, 2024

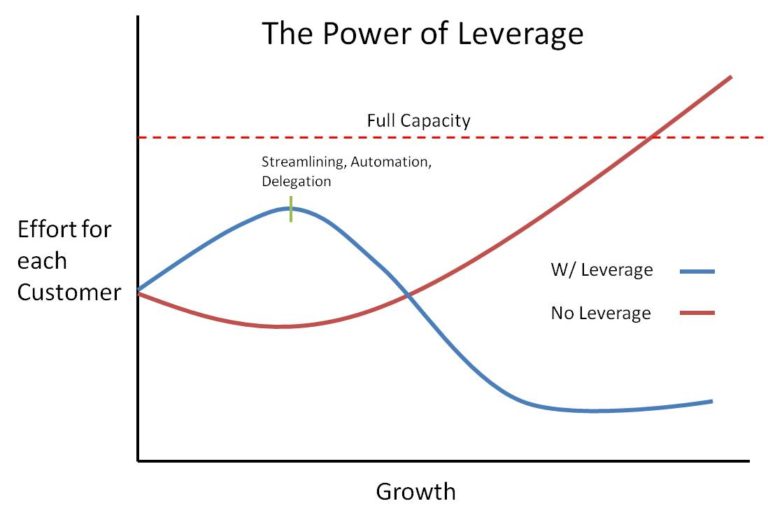

Financial advisers really need to invest more into their practices. Now. More money, more thinking, more strategy….more leverage. Even those who have been investing probably need to invest more.

Financial advisers really need to invest more into their practices. Now. More money, more thinking, more strategy….more leverage. Even those who have been investing probably need to invest more.

Comments (0)