Professional Services & Sales & Marketing for Professional Services & Strategic Issues & Strategy

A Value Creation Model For Advisory Firms

January 23, 2023

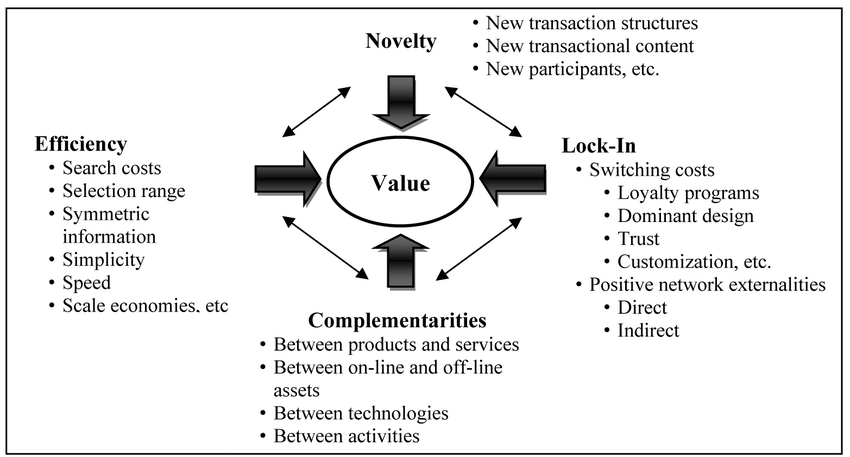

Challenging times test whether we are truly delivering value, and whether we have a good value creation model for the advisory firm. Is the practice focussed upon the areas where it can improve in its value delivery to clients…does it even know which areas they are?

Challenging times test whether we are truly delivering value, and whether we have a good value creation model for the advisory firm. Is the practice focussed upon the areas where it can improve in its value delivery to clients…does it even know which areas they are?

Comments (2)