by Tony Vidler ![]()

![]()

![]()

It seems to me that it is worth advisers asking themselves what their risk tolerance is as business owners given all the market and regulatory changes that have occurred in a reasonably short period of time. When contemplating what changes should be made in response to more regulatory reform or fundamental industry shifts the risk tolerance question should be the NEXT question after answering the “what do the new rules say I have to do?” question.

It seems to me that it is worth advisers asking themselves what their risk tolerance is as business owners given all the market and regulatory changes that have occurred in a reasonably short period of time. When contemplating what changes should be made in response to more regulatory reform or fundamental industry shifts the risk tolerance question should be the NEXT question after answering the “what do the new rules say I have to do?” question.

Clearly the first requirement when contemplating the impact of law changes on our business is to make sure we set up the systems and revise the processes that are necessary to be compliant at least. Compliance is the first objective…but it should not be the ultimate objective.

Moving beyond the necessary changes one must make in order to operate legally each advice business can take a number of strategic directions, and it is perhaps the risk tolerance of the owner or principals which best determines the right choice for them. The right choice of course may not be the path with the highest potential reward, because it isn’t just about ROI…which is exactly the same approach we advise clients, isn’t it?

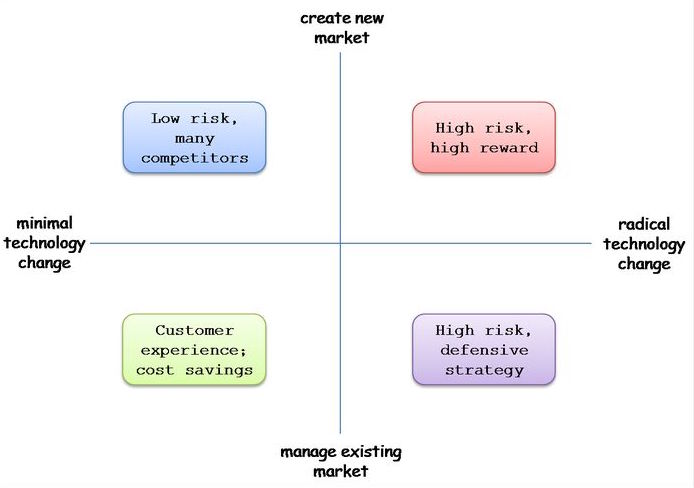

One must balance potential return or reward with what we are prepared to risk, and what we are prepared to invest. While there are many variables where one might invest time, capital or labour to grow a practice the toughest area for professionals to make these decisions is in the technology space, closely followed by staffing. The right mix of tech and people (or labour capacity) can be wildly different between advisers because of their risk tolerance. There are of course so many potential options to introduce efficiencies or reach brand new markets, or to do business in entirely different ways to how the professional services business has ever done it before, but many of them will be deemed high risk by some practitioners whereas others will see them as well worthwhile.

Choices, choices, choices…. and this is why it makes sense to consider your business risk tolerance alongside your strategic objectives just as you would when creating a plan for a client.

So when it comes to deciding how “radical” to get with your practice technology (investment) decisions are you conservative, balanced, moderately aggressive or aggressive? And then how does that fit in with possible strategic objectives?

For example:

The conservative option is to focus on retention of accounts and utilising existing and established technology – minimal disruption and minimal investment. A pretty safe place to be…for a while. At the other extreme if your desire was to break new ground and get to brand new markets in brand new ways, then it would make sense to consider investing heavily in different technology and delivery systems to get ahead of consumer trends. Be where they are going to be, and work how they are going to work, even though they aren’t doing it yet….but that is pretty risky, right? But the potential for exponential reward is worth it to some….

So which way is the right way to evolve your practice beyond making the necessary changes to comply depends on your risk tolerance really. When thinking strategically about the development of the business it is helpful to apply the same process you might to a client: once the rules of engagement have been established go straight to determining what is an acceptable level of risk before trying to design strategy.

You might also be interested in this related article:

Client Focus, or Compliance Focus?

Comments (0)