Advice Processes & Professional Services & Sales & Marketing for Professional Services

Good? Fast? or Cheap? What sort of advice is it going to be?

April 24, 2023

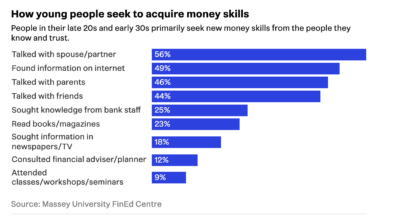

A few years ago a university in New Zealand conducted a study to find out where consumers were turning to for financial advice. At the time they found that the number one source of financial advice for most respondents was “newspapers and media”.

A few years ago a university in New Zealand conducted a study to find out where consumers were turning to for financial advice. At the time they found that the number one source of financial advice for most respondents was “newspapers and media”.

Comments (2)